Original article: Banco Central: inflación cae más rápido de lo esperado y se encamina a la meta de 3% a inicios de 2026

The Central Bank of Chile announced that inflation is decreasing more rapidly than anticipated and forecasts it will reach the 3% target by early 2026. This positive outlook comes as both the local and global economies perform slightly better than expected in September. The report challenges the narrative promoted by the far-right that «Chile is falling apart,» at least from an economic standpoint.

Inflation Falls Faster Than Expected, Approaching 3%

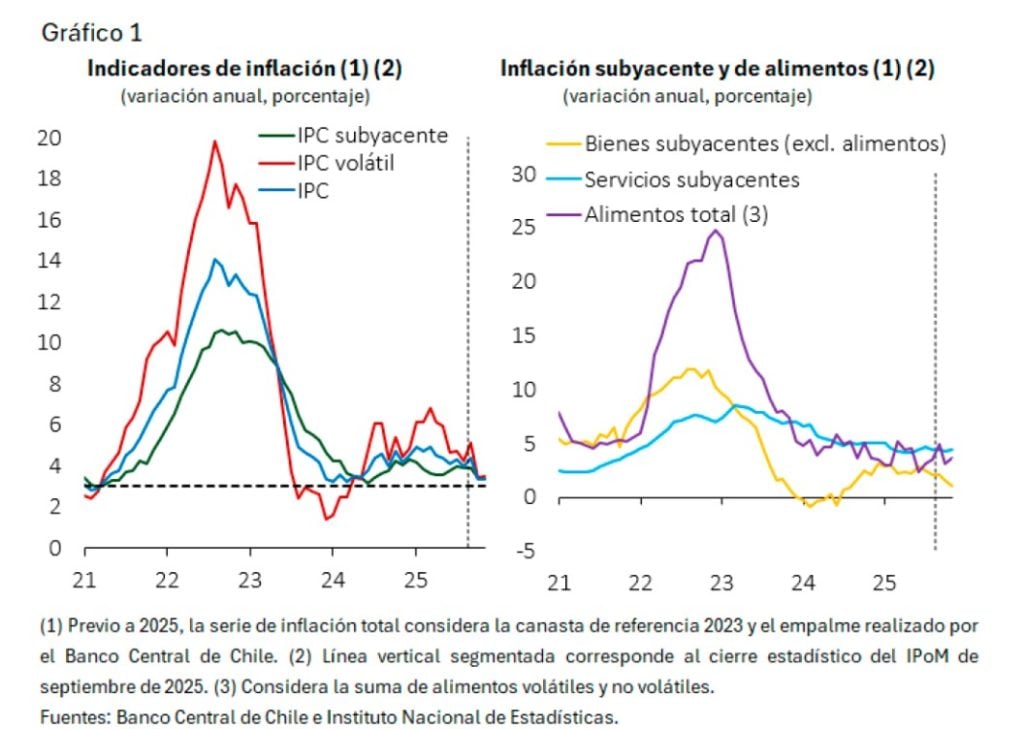

According to the Monetary Policy Report (IPoM) from December 2025, overall inflation has decreased more swiftly than projected in September, affecting both the general and core indicators. In November, the annual variation of the overall CPI and the CPI excluding volatile items was 3.4%, down from the nearly 4.0% observed in August.

The Central Bank notes that inflation expectations for two years remain at 3%, aligning with the official target. In the central scenario of the IPoM, inflation is expected to reach 3% in the first quarter of 2026 and remain around that level throughout the rest of the policy horizon.

The institution explains that inflation accumulated over the last four months was less than anticipated in the previous report, particularly due to the behavior of some cost factors. The difference was concentrated in goods, significantly influenced by the appreciation of the peso—over 4% since the last IPoM—and trade diversion effects impacting prices of certain imported products, alongside atypical behavior in some food items. In contrast, there were no major differences observed in services, although the growth in labor costs, despite slowing, remains above historical averages.

Economy Resilient Against Collapse: Dynamic Investment and GDP on Track

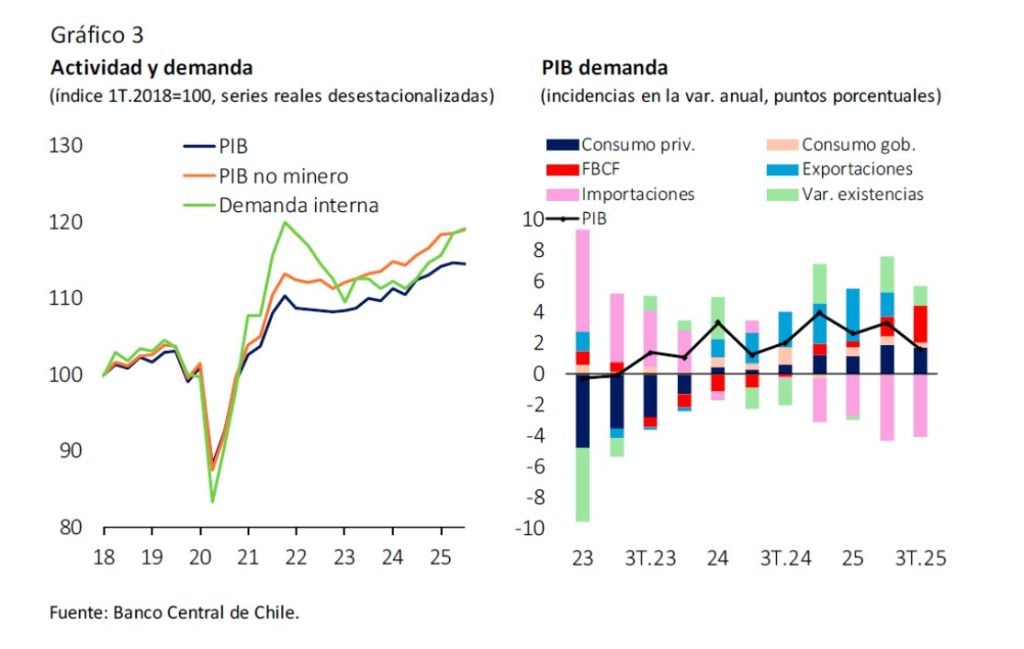

In contrast to the narrative of a perpetual crisis, the Central Bank asserts that, overall, local activity has aligned with expectations, exhibiting more dynamic investment, especially in machinery and equipment. In the third quarter, the non-mining GDP grew as projected: adjusted for seasonality, it increased by 0.4% quarterly (2.6% annual, original series), particularly boosted by the performance of services and, to a lesser extent, trade.

The total GDP did show a slight decrease of 0.1% quarterly (1.6% annual), primarily due to weak performance in the mining sector, impacted by reduced production in some operations and a lower ore grade. Within expenditure, the gross fixed capital formation (FBCF) in machinery and equipment saw above-expected growth, driven by mining and energy projects, while investment in construction remains lagging.

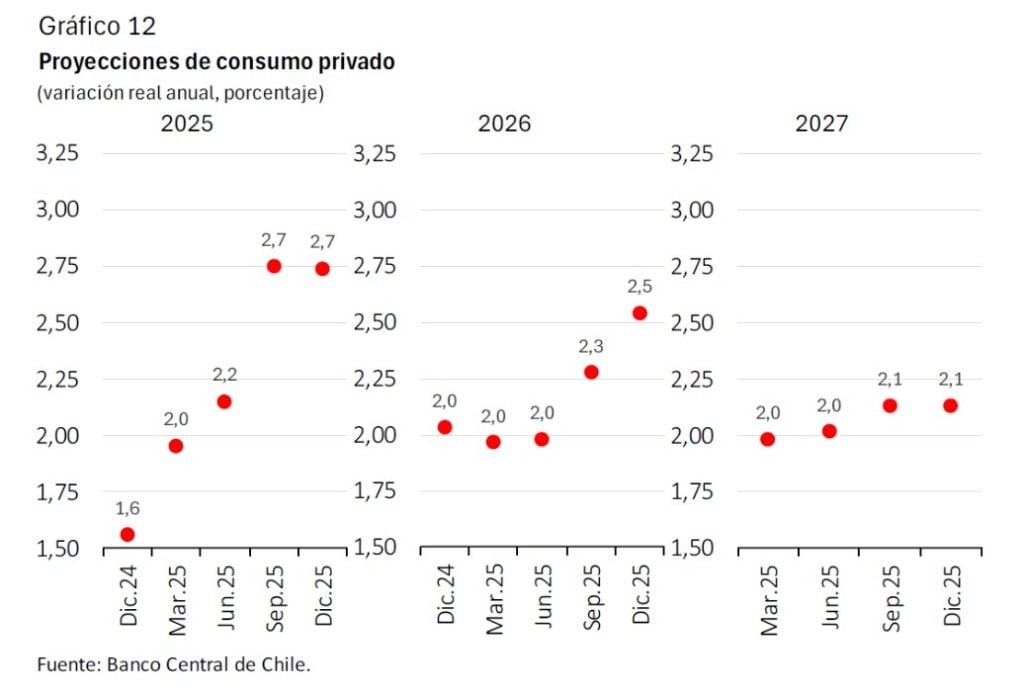

Private consumption performed in line with projections, exhibiting a slower quarterly growth rate compared to previous periods. Consumer expectations have improved, and the labor market shows signs of progress: the unemployment rate has dropped since the last IPoM in September, although it still exceeds historical averages, and job creation remains limited.

High Copper Prices, Greater External Momentum, and Persistent Risks

The report emphasizes that the external momentum for the Chilean economy is somewhat greater than previously forecasted in September. Global activity has proven more resilient than anticipated against early-year uncertainties, and global financial conditions have improved, marked by widespread stock market gains and interest rate cuts by the Federal Reserve, which are expected to continue into 2026.

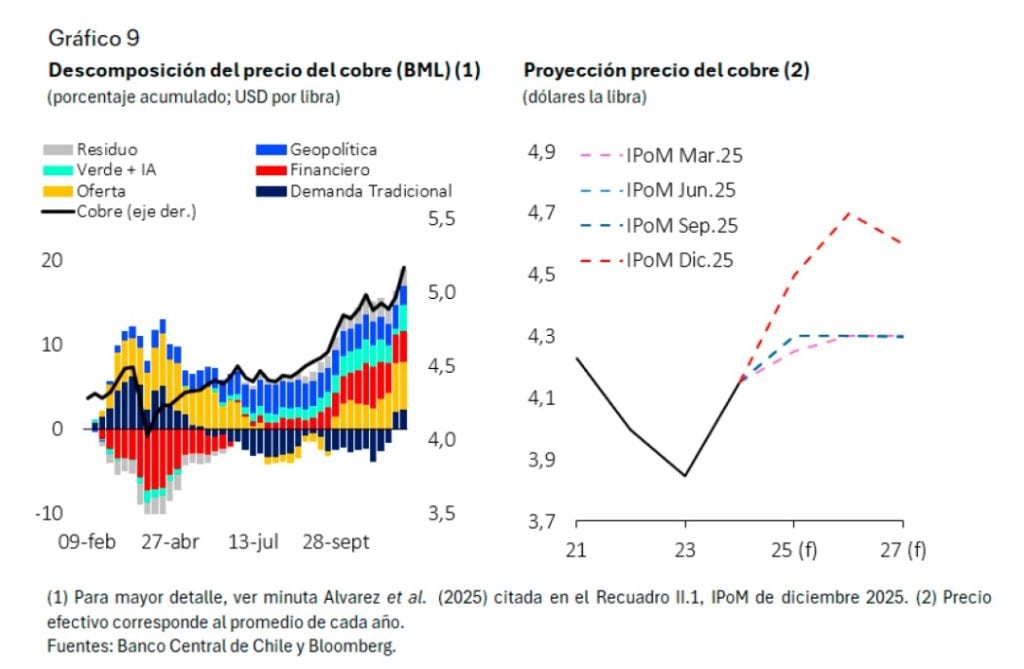

A crucial element for Chile is the improvement in terms of trade, particularly due to rising copper prices, which have surpassed $5 per pound. The Central Bank attributes this increase to supply issues and increased demand stemming from investments in artificial intelligence, energy transition, and defense spending. Simultaneously, oil prices have decreased, although refined products such as gasoline have not fallen as much as expected due to specific market factors.

In this context, the Central Bank has revised upward its growth forecast for trading partners, from an average of 2.6% to 2.8% for 2025-2026, and has updated its commodity price projections: the average copper price is now estimated at $4.7 in 2026 and $4.6 in 2027, higher than the previous forecast of $4.3. This contributes to a lower projected current account deficit.

Nonetheless, the report underscores that global risks remain high: geopolitical tensions persist, increased defense spending in developed economies may exacerbate their fiscal situations, and uncertainties loom over asset valuations linked to emerging technologies. Additionally, the Council warns of the risk of a sharp reversal in global financial conditions that could impact both external financing and commodity prices.

Growth Projections and Monetary Policy

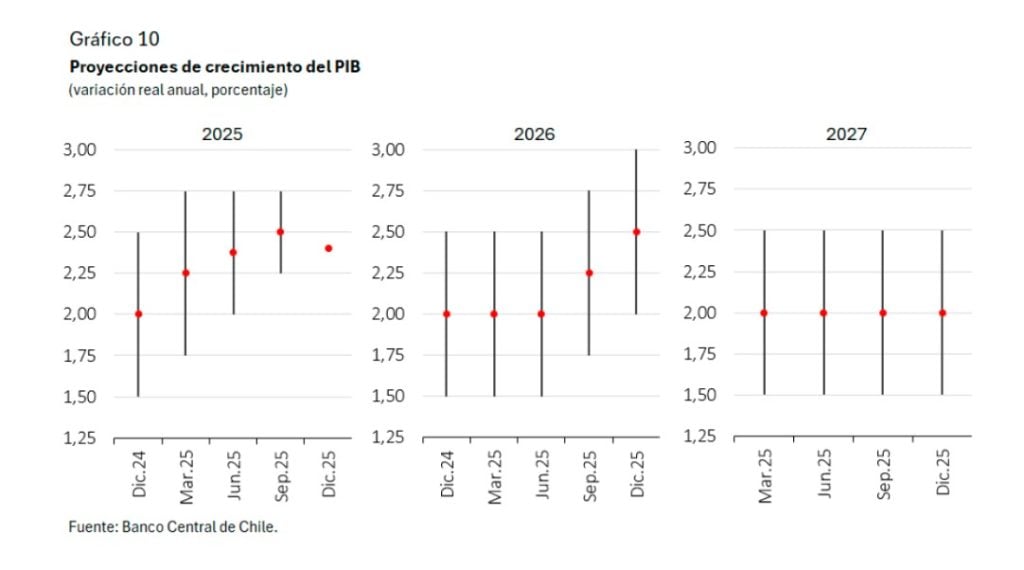

Overall, the Central Bank’s central scenario is more favorable than in the previous IPoM. For 2025, it estimates GDP growth at 2.4%, within the projected range from September (2.25-2.75%). For 2026, the range is revised upward to 2.0-3.0% (from 1.75-2.75% in September), while 2027 remains between 1.5 and 2.5%, consistent with the economy’s trend growth.

Investment (FBCF) also shows improved prospects: a growth of 7% is projected for 2025 and 4.9% for 2026 (compared to 5.5% and 4.3% in September), with an estimated 3.1% for 2027. The Central Bank highlights that financial conditions and business expectations have improved, and investment momentum is expected to become more widespread across sectors in the coming years. Private consumption is anticipated to approach rates consistent with trend GDP growth, with annual expansions near 2.5% in 2025 and 2026, and 2% in 2027, supported by consumer confidence and wage growth.

Regarding monetary policy, the Council emphasizes that inflation has decreased more rapidly than expected in September and that the goal is to ensure projected inflation remains at 3% over the two-year horizon. To achieve this, it will assess upcoming movements in the Policy Interest Rate (TPM) based on the macroeconomic scenario and its impact on inflation convergence, reaffirming its commitment to conducting policy flexibly.

Thus, while a narrative of economic catastrophe takes hold in some sectors, the Central Bank itself—despite all its nuances and warnings—presents a different picture: inflation is declining faster than expected and is on track to meet the 3% target, in an economy that, despite its problems, is far from «falling apart.»

View the full IPoM report from December 2025 from the Central Bank here:

Hazte socio 👍

Con tu donación aportas a la sostenibilidad económica y existencia de este medio.

Elige cómo quieres aportar a la existencia y financiamiento colectivo de este medio!

Reveniu

Reveniu

Relacionados

Central Bank Cuts Interest Rate to 4.5% Amid Rising Copper Prices and Improved Inflation Outlook

Hace 1 mes

Mesina Accuses Central Bank of Overreach: IPoM Wades Into Labor Policy Weeks Before Chile’s Elections

Hace 3 meses

Boric Shares Critical Remarks on Kast's Spokesperson Following Central Bank Projections

Hace 4 semanas